When the idea of expatriate life appeals to you, planning your social protection becomes important. Indeed, before taking the plunge, it’s important to consider your health insurance. The Caisse des Français de l’Etranger (CFE ) can be your ally in this quest for social security abroad.

CFE is here to help you stay healthy abroad, offering you social security coverage “à la française”. Whether you’re a salaried employee, self-employed, student or retired, CFE offers health cover solutions tailored to your profile.

However, it’s important to ask how CFE actually works. What cover does it offer? How do you select the coverage best suited to your needs? And, of course, how much will it cost? We’ll look at these points in detail in this article.

What is the Caisse des Français de l’Etranger (CFE)?

The Caisse des Français de l’Étranger (CFE) is much more than just an administrative body; it’s a true partner in your expatriation. Its main mission is to offer French nationals living outside France social protection comparable to that of the general French Social Security system.

Unlike the compulsory general scheme in France, CFE operates on a voluntary basis. You are free to choose whether or not to join CFE, depending on your needs.

CFE offers a wide range of benefits to cover your essential health, retirement and provident needs:

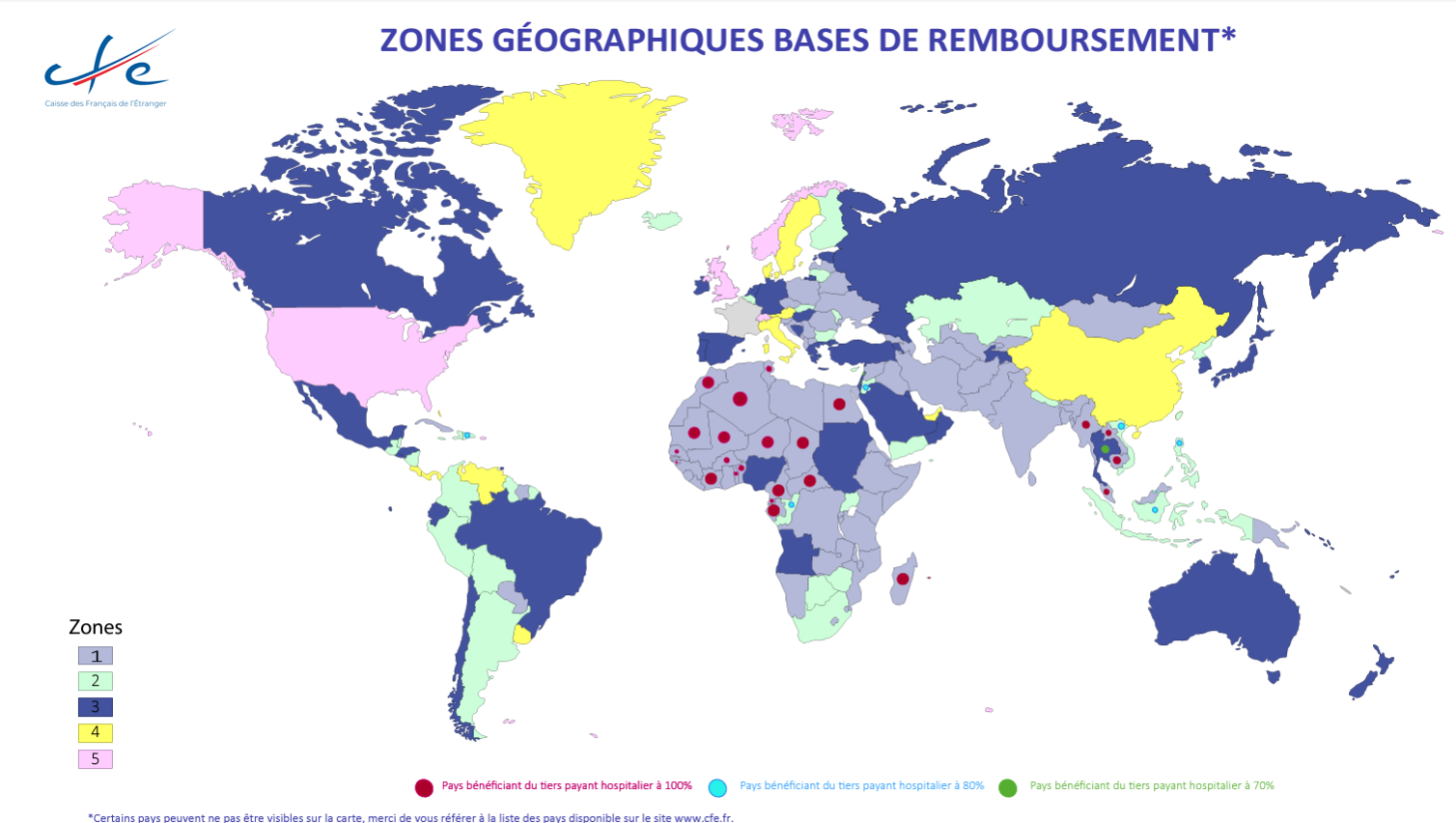

- Reimbursement of healthcare costs: From January 1, 2024, CFE has adjusted the distribution of countries within its five zones of coverage in response to rising global healthcare costs. Some destinations, such as Iraq, Chad and Russia, have been downgraded to less advantageous reimbursement zones. In all, eleven countries have been reclassified to a higher zone, which may influence the level of healthcare reimbursement depending on your country of residence. These changes can result in lower CFE reimbursements and higher out-of-pocket expenses for policyholders, making it all the more important to take out supplementary insurance for optimum coverage.

- Retirement: This allows you to contribute to your French retirement pension.

- Additional benefits: CFE also offers optional additional benefits (death, disability, incapacity for work).

CFE can be a major asset to your expatriation project.

How do I join CFE and choose my coverage?

Joining the CFE is both quick and easy, requiring only that you meet the eligibility conditions and follow the appropriate procedures.

Eligibility requirements and how to apply

To subscribe, all you need to do is meet the following criteria:

- French nationality.

- Not be (or no longer be) covered by the compulsory French Social Security system.

CFE is open to all French nationals planning to leave France or living abroad, whatever their situation: employee, self-employed, student, pensioner, etc. CFE membership requires no medical questionnaire, which ensures that your application is accepted. So you can join even if you have a medical history or chronic illness. What’s more, this has no impact on the amount of contributions you pay, or on the benefits you are covered for. CFE also offers the possibility of receiving daily allowances in the event of temporary or permanent stoppage of work.

Please note: CFE helps you preserve your pension rights. Thanks to its pension insurance, your individual account will be automatically updated, to top up your pension entitlements.

Joining CFE is easy, and can be done online or by post. All you need to do is complete an application form and provide the required supporting documents. Santexpat.fr’s international health experts can help you with the process of joining the Caisse des Français de l’étranger.

Santexpat.fr, la nouvelle façon de

s’assurer à l’étranger

1. Meilleurs prix

- Sans surcoût sur les tarifs assureurs,

nous comparons + de 300 offres d’assurance

2. Simplicité

- Un parcours simple pour sélectionner votre

solution en quelques clics

3. Accompagnement

- Nos conseillers sont là pour un

accompagnement 100% personnalisé

Choosing your health cover

CFE offers several membership options depending on your status: student, adult, retired, family or solo. Here’s an overview of the main insurance options offered by CFE.

- Professional Risks Insurance: Designed for expatriate employees, this insurance offers protection in the event of accident or illness while working, with benefits comparable to those provided by Social Security in France. Paid interns and students can also benefit.

- CFE Retraite insurance: This allows you to benefit from a pension without losing the years spent abroad. It is aimed at employees, people with families and former employees of a compulsory French scheme.

- Assurance Maladie, Maternité et Invalidité (Health, Maternity and Disability Insurance): This offers coverage comparable to that provided by the Caisse Primaire d’Assurance Maladie (CPAM) in France for all medical procedures. It offers five types of contract to suit different needs: MondExpat Santé, JeunExpat Santé, RetraitExpat Santé, FrancExpat Santé, and EmiratExpat Santé.

Once you have subscribed to one of CFE’s offers, you can manage your account and track your reimbursements on your personal space(CFE mon compte).

CFE at your side when you return to France

It’s worth mentioning that CFE issues its policyholders with a Carte Vitale, which is extremely practical when they return to France. The Carte Vitale gives policyholders simplified access to healthcare in France. This simplifies administrative procedures and reimbursements. Policyholders can be reimbursed for their medical expenses more quickly, which is a significant advantage.

How much does it cost to join the CFE (Caisse des Français de l’étranger)?

The cost of CFE membership depends on several factors. Firstly, your age influences the amount of your contributions, which increase with age. What’s more, your income may also be taken into account in the calculation of contributions, depending on the membership formula you choose. The guarantees you select will also have an impact on the cost of your membership: more extensive coverage generally entails higher contributions. What’s more, you have the option of splitting your contributions over a period of 12 to 36 months, at an additional cost. To estimate premiums and compare offers. You can use the Santexpat.fr comparator, which will show you rates at the first euro or in addition to CFE.

If you wish to take out a CFE-affiliated health insurance policy, we advise you to start the process as soon as possible, as there is a waiting period if you sign up more than 3 months after leaving France. This waiting period is 3 months for people under 45 and 6 months for those over 45. Finally, CFE membership does not exempt you from paying contributions to the compulsory schemes in your country of residence.

CFE rates in 2024: Changes for expatriates

CFE contributions for expatriates underwent a significant increase in 2024. From April 1, 2024, a 5.4% increase in rates was applied, in line with the trend in global healthcare spending. New age brackets have also been introduced, to better spread the costs associated with aging. For example, a young expatriate under the age of 30 will now pay around €152 per quarter, whereas a policyholder aged 60 or over could see his or her contribution rise to €727 for individual cover. This increase is in addition to the abolition of the loyalty bonus, a 5% reduction granted to members according to their length of service, which has no longer been applied since January 1, 2024.

Supplementary health insurance: Optimize your expatriate protection

Recent changes to CFE coverage and rates have made supplementary health insurance even more essential to fill any gaps. The reduction in CFE coverage can lead to an increase in supplementary health insurance premiums, which are required to cover a larger share of healthcare costs. With complementary health insurance, you benefit from full reimbursement of your medical expenses. It also covers specific treatments and procedures that the CFE might exclude. It offers you comprehensive coverage for your healthcare needs abroad.

CFE, a health ally for your expatriation

CFE can help you benefit from French-style social protection. It’s important to remember that CFE does not cover all your expenses. So, a complementary health insurance plan seems compulsory to benefit from 100% reimbursements.

Some of the insurers we work with offer a teletransmission system with the CFE, so you can benefit from easier management and a single reimbursement. Depending on your destination abroad and your profile, it may be worthwhile to take out expatriate health insurance in addition to CFE. In some cases, however, it may be more advantageous to opt for first-euro coverage. Our international health experts will study your situation with you to find the solution best suited to your needs.